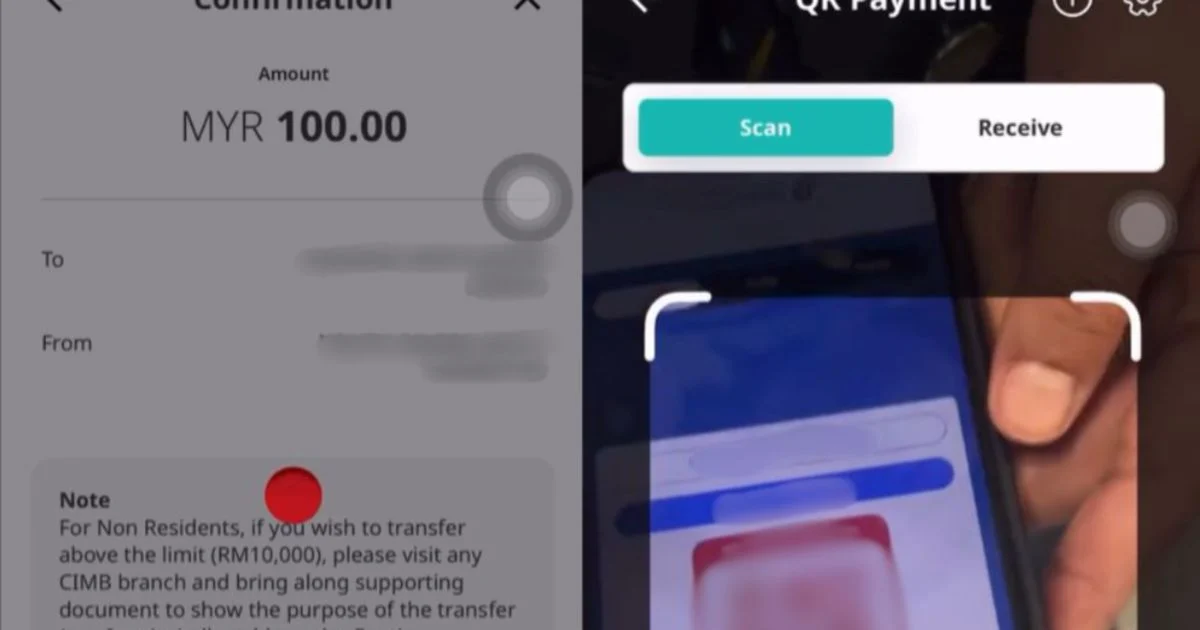

The Malaysian Border Control and Protection Agency has launched a formal internal investigation following allegations that one of its officers stationed at Kuala Lumpur International Airport's Terminal 2 accepted a RM100 payment through a personal Quick Response code transaction. The development marks another chapter in ongoing scrutiny of financial practices among airport immigration and border control personnel, who occupy a critical position in Malaysia's travel and trade infrastructure.

The incident highlights the vulnerability of digital payment systems to misuse in high-traffic immigration environments. Personal QR codes have become ubiquitous in Malaysia's cashless economy, enabling rapid peer-to-peer transfers through mobile applications. However, their ease and informality make them a potential vector for unofficial payments, particularly in settings where travellers may feel compelled to expedite document processing or resolve administrative queries through informal channels. The allegation suggests that at least one officer may have leveraged this accessibility inappropriately during routine border operations.

KLIA Terminal 2 processes approximately 35 million passengers annually, making it Southeast Asia's third-busiest aviation hub and a critical node in regional travel networks. The concentration of immigration processing at such facilities creates inherent compliance challenges. Border control agencies worldwide face the perpetual tension between maintaining efficient passenger flow and preventing corruption, a balance that Malaysian authorities have struggled with periodically. The emergence of digital payment allegations at KLIA specifically underscores how modern financial technologies can outpace institutional safeguards designed for traditional cash-based misconduct.

The MCBA's decision to investigate signals institutional awareness of the reputational stakes involved. A single unaddressed allegation can erode public confidence in border security mechanisms during an era when Malaysia seeks to position itself as a premium travel destination and financial hub. International travellers and Malaysian expatriates using KLIA rely on the integrity of immigration processes, and perceptions of petty corruption at entry points can influence both tourist arrivals and business confidence. The agency's rapid response therefore serves both disciplinary and preventative purposes.

Institutional corruption involving border personnel carries particular weight because these officials operate at the threshold of national sovereignty and economic engagement. Unlike misconduct in purely domestic contexts, border-level malfeasance can facilitate human trafficking, smuggling, and security evasion, creating cascading risks beyond the immediate financial impropriety. A RM100 personal transfer might appear trivial in isolation, but it represents a breakdown in procedural integrity that, if systemic, could compromise border security fundamentals. This distinction likely informed the MCBA's decision to treat the allegation seriously despite its modest financial dimensions.

The proliferation of digital payment methods in Malaysia has created new enforcement frontiers for anti-corruption bodies. Traditional graft detection mechanisms—surveillance of cash transactions, documentation of irregular expenditures—translate imperfectly to QR-code mediated transfers, which leave minimal institutional trace unless specifically flagged by banking systems or reported by complainants. The informality that makes QR codes convenient for legitimate commerce equally facilitates informal payments that evade conventional auditing. The MCBA investigation will necessarily involve examining banking records, transaction logs, and mobile payment application data to reconstruct the alleged transfer's circumstances and verify whether systemic vulnerabilities enabled the misconduct.

This episode also reflects broader vulnerabilities in Malaysia's public sector accountability infrastructure. Immigration and customs agencies across Southeast Asia face persistent corruption challenges, reflecting both insufficient training in ethics and inadequate institutional oversight mechanisms. Personnel at visa and border control checkpoints frequently encounter travellers willing to pay unofficial fees to circumvent waiting periods or regulatory compliance steps. Digital payment technologies have simultaneously expanded both legitimate and illegitimate transaction possibilities in these environments. Malaysian authorities' response to this allegation will signal their commitment to evolving enforcement capabilities in line with technological change.

The investigation's outcome will carry implications for MCBA's operational protocols and staff training frameworks. If substantiated, the allegation would justify increased scrutiny of officer financial disclosures, restrictions on personal mobile payment use during duty hours, or enhanced monitoring of passenger complaints. Conversely, if investigation reveals that the complainant misinterpreted ordinary administrative interactions, the incident still provides valuable intelligence about vulnerability perceptions among airport users. Either outcome should inform revised procedures that address the specific pathways through which modern payment systems might facilitate misconduct.

For Malaysian travellers and businesses, the MCBA's investigative response offers limited but meaningful reassurance. Institutional investigations, even when publicised, demonstrate that corruption allegations receive scrutiny rather than silent dismissal. However, the investigation's ultimate effectiveness depends on whether findings result in disciplinary action, policy revision, and public accountability—transparency dimensions that Malaysian authorities have inconsistently demonstrated in comparable past cases. The agency's handling of this matter will become a benchmark against which future border security integrity claims are assessed by both domestic and international observers.